Introduction

Significant changes have occurred in the postal sector across Europe. Partly as a result of the covid-19 pandemic and partly due to technological evolution, letter deliveries have declined precipitously while parcel deliveries have increased substantially. At the same time digital mail has become ubiquitous. For example, in early March 2025, NordPost, the postal incumbent in Denmark and Sweden announced that after 400 years of providing regular postal delivery it would cease collecting and delivering letters.

The consequence of these changes in technology and consumer habits is that the cost of simple postal services has become commercially unviable. It means that the compensation for public service obligations has had to increase.

A case in point in a recent Commission decision – SA.104103 – authorising compensation to Czech Post – the main postal operator in the Czech Republic – for the provision of the universal postal service obligation [USO] over the 2023-2024. In this case, in addition to postal services, Czech Post also provides other services, such as financial services [e.g. banking, cash services] and payment of pensions.

Czech Post has been entrusted with a postal USO by Czech Telecommunications Office [CTO] which is the national regulator for post and telecoms. The USO concerns the delivery of postal items up to two kg; delivery of postal parcels up to ten kg; free delivery of postal items up to seven kg for blind persons; and the delivery of certain other items such as those defined by the Universal Postal Union. As a universal service provider, Czech Post is obliged to ensure accessibility to the specified postal services, at affordable prices, throughout the whole territory of the country, and at least once every working day.

Databoxes Information System [DBIS]

In addition to being entrusted with the USO, Czech Post is also entrusted with the provision of DBIS which is an electronic channel for internal communication within the public administration and for secure communication between the public administration and citizens and companies, which, in some cases, replaces conventional postal services such as registered post.

In July 2024, the Commission adopted a decision [SA.109072] concluding that the compensation to be granted to Czech Post for the delivery of DBIS over the period 2023-2027 [CZK 4 billion, approximately EUR 160 million] constitutes aid compatible with the internal market on the basis of Article 106 (2) TFEU. This decision was reviewed here on 29 October 2024. It can be accessed at: https://www.lexxion.eu/stateaidpost/an-unusual-sgei/

Cost allocation methodology

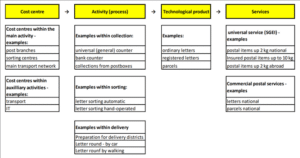

“(24) Czech Post is required to keep separate accounts of costs and revenues associated with the provision of individual services included in the scope of the USO for which it is designated […] and of other services, which are audited annually by an independent auditor. In particular, this separate accounting system and cost allocation follow the Activity-Based Costing (ABC) method, where costs are assigned to cost centres, such as post offices, depots, and sorting centres, based on individual activities that can be tracked separately; cost items that are not recorded at operating cost centres (e.g., VAT, overhead) are allocated according to pre-approved rules, in proportion to the allocation of direct costs.”

Amount of aid

“(27) The compensation to be granted to Czech Post will depend on the net costs of the USO, as defined by the Czech authorities, and verified by CTO, and is limited to a maximum amount of CZK 1 500 million (approximately EUR 59 million) each year to be paid out of the State budget.”

Methodology for determining the net USO cost

“(33) In order to determine the net cost, CTO uses a methodology based on the net avoided costs, in order to determine the net cost for the provision of the USO SGEIs, as the difference between Czech Post operating with such obligations and net cost of operating without such obligations. For this purpose, CTO has taken into consideration in the factual scenario that Czech Post is entrusted with both the DBIS and the USO SGEIs. In the counterfactual scenario, Czech Post is not entrusted with either of these services. The methodology determines the net cost for the provision of the USO SGEIs, while the net cost for the DBIS SGEI is covered by the DBIS Decision.” The net cost for the DBIS SGEI is here indicated as the public service obligation [PSO] and the corresponding public service compensation [PSC].

The difference between the factual and counterfactual scenarios is calculated in five steps. Paragraphs 36-45 of the decision define and explain the components of the five steps.

Step 1: Define the Factual Scenario:

It describes the actual situation in which Czech Post is obliged to provide the USO and the DBIS.

Step 2: Define the Counterfactual Scenario:

The counterfactual scenario is always more difficult to define because it is hypothetical. It seeks to identify the services that are economically viable in the absence of any obligations imposed by the state. The main elements of the factual scenario that would change in the counterfactual scenario and that are limited to the USO network (while the rest of Czech Post’s network and operations would not be changed) include:

- Termination of DBIS activities.

- Reduction of postal branches [about 2000 branches would be closed].

- Less frequent deliveries [no more daily deliveries].

- Termination of other unprofitable services.

Step 3: Assess intangible benefits and market advantages:

In the counterfactual scenario Czech Post would forfeit certain intangible and market benefits associated with its role as the designated USP. They are as follows:

- Brand value: The postal licence holder is well-known to consumers. “However, Czech Post argues that the USO no longer contributes significantly to enhancing its brand value.”

- Exclusive right to sell postage stamps and philately items which generates extra revenue.

- Enhanced advertising effects: This benefit arises from Czech Post’s ability to use its property, such as vehicles and buildings, for marketing purposes.

- VAT exemption: The VAT exemption for universal services enables Czech Post to reduce the effective price for those services.

Step 4: Determine the reasonable profit:

The reasonable profit is calculated as the difference in capital costs between the factual and counterfactual scenarios. It is based on an assessment of the cost of capital based on the capital employed and the Weighted Average Cost of Capital [WACC] in both scenarios.

Step 5: Identify the net cost of the USO and amount of compensation:

The net cost is the difference between the factual and counterfactual scenarios [i.e. the difference between avoidable costs and foregone revenue], minus the value of intangible and other market benefits. The estimated reasonable profit is then added to the total net cost. The final step in determining compensation involves comparing the net cost of the USO with the “unfair burden cap” set in the Postal Services Act. If the net cost exceeds the statutory limit, the compensation amount is capped at CZK 1 500 million per year.

Presence and compatibility of the aid [PSC] with the internal market

The Commission concluded that the PSC constituted State aid because it satisfied all of the criteria of Article 107(1) TFEU, while it failed to conform with all of the Altmark conditions. In particular it failed the fourth Altmark condition. Czech Post was the only participant in a procurement procedure and no comparative costing had been attempted to prove the efficiency of Czech Post.

The Commission assessed the compatibility of the aid in accordance with the 2012 SGEI Framework. Since the annual compensation was about EUR 59 million, it exceeded the threshold of EUR 15 million laid down in Commission Decision 2012/21 which functions as a block exemption for SGEI aid.

The Commission examined and confirmed the following:

1) The USO concerned a genuine service of general economic interest and a public consultation had been carried out before the obligation was imposed, which established the need for a public service.

2) The USO was entrusted through a public act which defined the method for the calculation of the PSC.

3) The period of entrustment did not exceed the period required for the depreciation of the most significant assets required to provide the SGEI.

4) Cost allocation. The SGEI Framework requires that where an undertaking carries out activities falling both inside and outside the scope of the SGEI, the internal accounts must show separately the costs and revenues associated with the SGEI and those of the other services. This was true of Czech Post. The Commission decision also shows how the cost allocation is carried out in practice.

Fig 1: Cost allocation

5) Compliance with EU public procurement rules. The CTO carried out a public procurement procedure that defined certain eligibility criteria which were as follows: Any postal operator could participate if it “(127) (a) is authorised to conduct business in the field of postal services, (b) has technical capacity regarding its network of post offices and network of distribution centres to provide the USO, or indicates a method to ensure the operation by 1 January 2023 of the capacity to operate such networks, (c) provides appropriate evidence demonstrating that it has sufficient financial capacity for the operation of such networks, (d) possesses sufficient financial, technical and professional capacity to fulfil the USO, (e) has no financial, tax, insurance arrears and is not in a situation of insolvency, and (f) is able to provide a method for calculating the annual net cost of compliance with the USO, in accordance with Section 34b of the Postal Services Act and with Decree No 466/2012.” The Commission considered that “(128) the abovementioned requirements to be objective and proportionate to the needs related to the provision of the USO. The selection procedure imposed minimal requirements ensuring that the operator will have the capacity to deliver the services needed (i.e., the USO). The Commission believes that the selection procedure was sufficiently open and non-discriminatory as to allow postal operators to participate in the procurement procedure since all operators authorised to provide postal services could apply, to the extent that they demonstrated their capacity to deliver the USO.” “(132) The Commission also finds that the design of the procurement was made in line with the requirements of Directive 2014/24/EU.”

6) Absence of discrimination. Since there was no other SGEI provider, the PSC did not discriminate between undertakings.

7) Calculation of the net cost of the Universal Postal Service and amount of compensation. The Commission agreed with the elements of the net avoidable cost [NAC] methodology and the results of the calculations.

8) Verification of the absence of overcompensation. The CTO would carry out ex post checks to verify the veracity of the claims made by Czech Post.

9) Transparency. The Czech Republic committed to publish all the relevant information.

Conclusion

Since the Commission confirmed that the aid in question conformed with the requirements of the SGEI Framework, it authorised the measure.